You have two choices: in one corner, there’s Kuda, the sleek minimalist champion, promising transparency and budgeting aid. On the other hand, OPay, the feature-packed juggernaut, boasts affordability and diverse functionalities. Both are vying for your financial trust, both promise to revolutionize your money game. But who gets your fintech trust between Kuda vs Opay?

To help you make that informed decision tailored to your financial lifestyle, this comparison critically explores Kuda and OPay, dissecting their features, fees, security, and brand values.

We’ll also compare savings options, investment opportunities, and user interfaces, leaving no stone (or Naira) unturned.

So, whether you’re a penny-pinching pragmatist, a feature-hungry explorer, or simply overwhelmed by the fintech options, this comprehensive guide will equip you with the knowledge to achieve financial freedom with the ideal fintech.

Before diving into the comparison, let’s introspect. Ask yourself these excellent questions to kickstart your self-evaluation before choosing between Kuda and OPay. To personalize your journey, consider expanding on these points:

1. Financial Needs

Spending Habits: Track your expenses for a month to understand your spending patterns. Are you a big spender or someone who prioritizes saving?

Income Sources: Do you have a regular income? Do you receive freelance payments or rely on irregular income sources?

Financial Goals: Do you have short-term goals like managing daily expenses or long-term aspirations like saving for a house or retirement?

2. Priorities

Fees: Are you highly sensitive to transaction charges and ATM withdrawal fees? Or are you willing to pay slightly more for additional features or convenience?

Features: Do you need basic functionalities like transfers and bill payments, or are you looking for advanced features like investment options, budgeting tools, or cryptocurrency capabilities?

User Experience: How important are a user-friendly app interface and responsive customer support to you?

3. Customer Support

Preferred Communication Channels: Do you prefer in-app chat support, email correspondence, or the option to speak with a live representative over the phone?

Response Time: How quickly do you expect your queries to be resolved?

4. Additional Personalization

Tech Savviness: Are you comfortable navigating mobile apps and using various financial features, or do you prefer a simpler, more basic platform?

Brand Values: Do you align with the brand image and values of each platform? Consider their approach to transparency, sustainability, and social responsibility.

Pros and Cons of Kuda

Kuda has proven to be a prominent player in the Nigerian fintech space, known for its user-friendly app, innovative features, and focus on transparency. However, like any platform, it has its strengths and weaknesses. Let’s see the pros and cons of Kuda to help you decide if it’s the right fit for you.

Pros

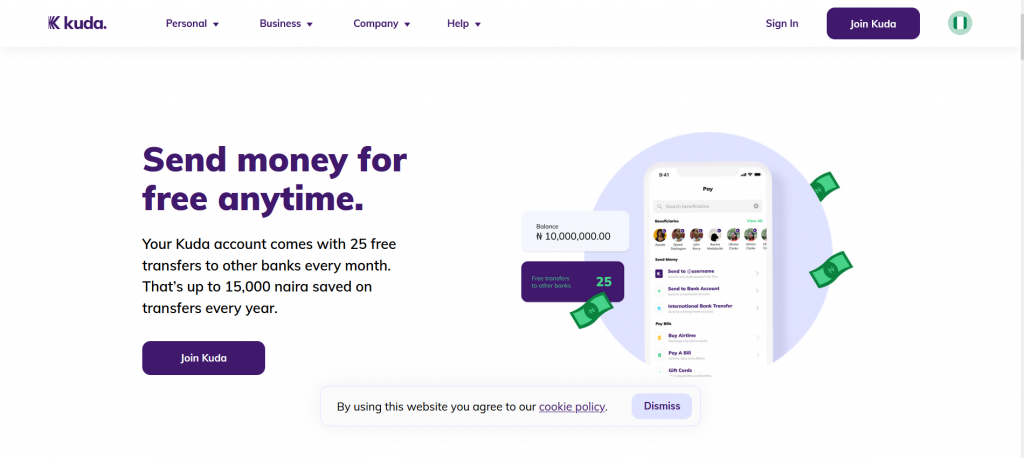

Free Transfers: Kuda offers free transfers between Kuda accounts and up to 25 free transfers to other banks every month, minimizing transaction costs. Extra transfers to other banks cost ₦10 each.

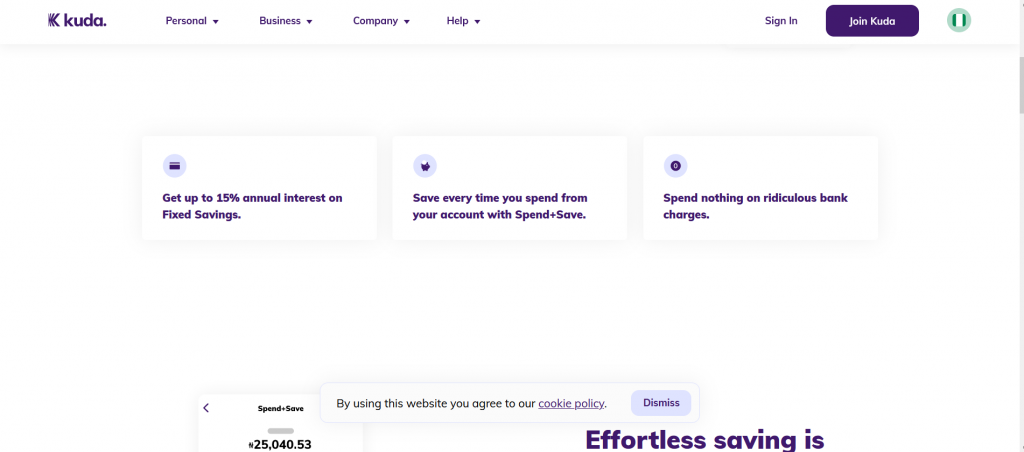

Savings Features: Kuda boasts “Goals” and “Target Savings” options, allowing users to set personalized saving targets and track their progress conveniently.

Fractional Stock Investing: Kuda stands out with its fractional stock buying feature, making investing in US stocks more accessible for users with smaller budgets.

Budgeting Tools:Budget on Kuda provides built-in budgeting tools and spending trackers, empowering users to monitor their expenses and manage their finances effectively.

User-Friendly App: The app is known for its clean and intuitive interface, so it is easy to navigate and use various features.

Customer Support: It offers in-app chat and dedicated phone support, ensuring prompt assistance whenever users encounter issues.

Transparency: Kuda has garnered a reputation for transparency in its operations and communication with users, fostering trust and building a positive brand image.

Cons

Limited Investment Options: While Kuda offers fractional stock buying, its overall investment options are currently limited compared to dedicated investment platforms.

International Transaction Fees: International transactions on Kuda incur fees, which might be a drawback for frequent international users.

Lower Interest Rates:Kuda’s savings features generally offer lower interest rates compared to some competitors, although this might be balanced by its free transfer benefits.

Brand Newcomer: Compared to established players like OPay, Kuda has a shorter track record in the market, which might make some users cautious.

Limited Physical Presence: Kuda primarily operates through its mobile app and lacks a widespread network of physical branches, which might be inconvenient for users who prefer in-person interactions.

Overall

Kuda is a compelling fintech for Nigerian users seeking a user-friendly platform with free transfers, budgeting tools, and innovative features like fractional stock buying.

However, its limited investment options, international transaction fees, and lower interest rates compared to some competitors should be considered. Weighing the pros and cons against your individual needs and priorities will help you determine if Kuda is the perfect fit for your financial journey.

OPay has made a significant mark in the Nigerian fintech landscape, attracting users with its diverse features, extensive merchant network, and focus on accessibility. However, OPay has its share of advantages and disadvantages. Let’s explore both sides of the coin to help you decide if OPay aligns with your financial needs

Pros

Wide Range of Features: OPay goes beyond basic banking, offering airtime purchases, bill payments, cryptocurrency buying, investments in fixed-income securities, and even ride-hailing and food delivery services within its app, creating a one-stop solution for various financial needs.

Extensive Merchant Network: They boast a vast network of over 300,000 partnered merchants, allowing users to make convenient payments at numerous stores and businesses across Nigeria.

Competitive Fees: While there are fees for some transactions, they are generally competitive compared to other fintechs, and users can benefit from freebies and cashback offers.

User-Friendly App: The app is known for its user-friendly interface and easy navigation, making it accessible to individuals with varying levels of tech savvy.

Growth and Innovation: OPay has established itself as a dynamic player in the fintech scene, constantly innovating and introducing new features, catering to users’ evolving needs.

Physical Presence: Unlike some purely digital platforms, OPay has a network of physical agents across Nigeria, providing support and assistance to users who prefer in-person interactions.

Cons

Data Privacy Concerns: OPay has faced public criticism in the past regarding data privacy issues, although they have taken steps to address these concerns.

Transaction Fees: While some transactions are free, others incur fees, and the fee structure can be complex, requiring careful attention to avoid unexpected charges.

Limited Savings Options: OPay’s savings features are currently less developed compared to competitors like Kuda, offering lower interest rates and fewer customization options.

Limited Investment Choices: Though OPay offers fixed-income investment options, OPay’s investment menu is currently more limited compared to dedicated investment platforms.

Customer Support: OPay primarily relies on email and FAQs for customer support, which might be less convenient compared to in-app chat or phone support offered by some competitors.

Overall

OPay presents a compelling option for fintech users seeking a feature-rich platform with an extensive merchant network for convenient payments and access to various financial services. However, concerns about data privacy, complex fee structures, and limited savings and investment options might be drawbacks for some users.

Evaluating both the pros and cons against your priorities will help you determine if OPay aligns with your financial goals and offers the right balance of features and convenience for your needs.

Kuda vs Opay: Head-to-Head Comparison

Let’s compare these fintech platform, considering core features, including:

1. Account Features

Here are some additional details for a more comprehensive comparison:

1. Account Features

a) Account Types

Joint Accounts: Kuda has the edge here, offering joint accounts ideal for couples or businesses with shared finances. OPay currently doesn’t provide this option.

Business Accounts: Both platforms cater to businesses, but the specific features and requirements might differ. Consider your business size, type, and transaction volume when choosing. Bigger businesses maximize the services of Kuda.

b) Savings Features

Interest Rates: Compare the actual interest rates offered by each platform for their respective savings features. Both Kuda and OPay offer tiered interest rates at 15% per annum based on the amount and duration of savings.

Flexibility: Kuda’s “Goals” and “Target Savings” offer more flexibility for personalized saving targets and easier access to funds. OPay’s “Savings Lock” restricts access for a set period, which might be beneficial for some users seeking stricter saving discipline.

c) Investment Options:

Fractional Stock Buying: Kuda stands out with its ability to buy fractions of US stocks, making investing more accessible for individuals with smaller budgets. OPay currently doesn’t offer this feature.

Investment Variety: OPay focuses on fixed-income securities, which can be less risky but also offer lower potential returns. Kuda’s “Jar” investment plans provide some diversity with thematic investment options, but the overall selection is currently limited compared to dedicated investment platforms.

Minimum Investment Amounts: With Kuda, you can deposit a minimum of $20 in your trading account and withdraw a minimum of $10 from your trading account. Also, you can buy or sell a minimum of $10 at once.

2. Transaction Charges

These are the transaction charges for the Opay vs Kuda comparison:

Transaction fees can significantly impact your overall financial experience. Let’s see the fee structures of Kuda and OPay:

a) Transfers:

Free Transfers: Kuda generally offers free transfers between Kuda accounts and up to 25 free transfers to other banks every month, minimizing transaction costs. Extra transfers to other banks cost ₦10 each. OPay charges fees for transfers to other banks; for ₦5,000 and below there is a ₦10 charge per transaction, between ₦5,001 and ₦50,000, ₦25 charge per transaction, and for ₦50,000 and above, ₦50 per transaction.

International Transfers: Both platforms charge fees for international transfers. Kuda charges a service fee of £3 for each transfer to Nigeria. As OPay has announced a partnership with leading global digital payments platform, WorldRemit, they offer international money transfers directly into OPay mobile wallets in Nigeria.So, you compare their specific rates and recipient countries supported to find the most cost-effective option for your needs.

Bill Payments: Kuda charges up to ₦100 per bill. This could be a deciding factor if you frequently pay bills through your fintech app.

b) ATM Withdrawals:

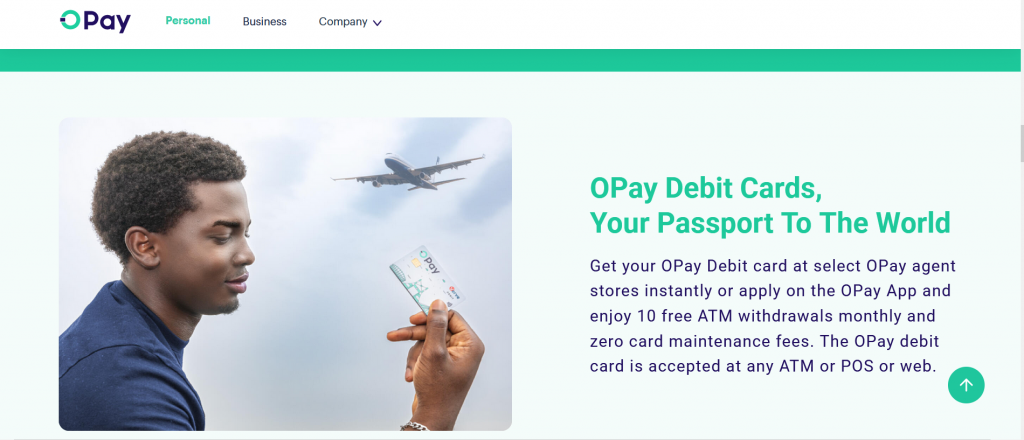

Free Withdrawals: Kuda allows you to withdraw cash at ATMs across Nigeria for free up to three times a month. With the OPay Debit card, you’ll enjoy 10 free ATM withdrawals monthly and zero card maintenance fees.

Withdrawal Fees: After exceeding your free withdrawals with Kuda, ATM providers will charge you the standard 35 naira withdrawal fee for the rest of that month. With OPay, cash withdrawals via ATM and POS are now limited to N500,000 weekly, after which there is a 3% processing fee. Consider your average monthly withdrawal frequency and preferred ATM locations when making your choice.

Starting today, cash withdrawals via ATM and POS are now limited to N500,000 weekly. Please note that any cash withdrawal above the limit will attract a 3% processing fee.

To avoid restrictions, perform more transactions on OPay and enjoy free and limitless transfers. pic.twitter.com/u0sxyRGaMZ

Design: While Kuda’s minimalist design appeals to users who prioritize simplicity and ease of navigation, OPay’s feature-rich interface might be more suitable for those who want readily accessible functionalities at their fingertips.

Features Accessibility: Analyze how easily you can find and utilize the features you need most frequently on each app. Pay attention to the menu structure, search functionality, and overall intuitiveness of navigating the features.

Customization: Check if either platform offers options to personalize the app interface or display preferences to suit your individual needs and preferences.

b). Customer Support

Response Time and Availability: Consider how quickly you expect your queries to be resolved and the channels you prefer for communication (in-app chat, phone, email). Kuda’s in-app chat and dedicated phone support offer faster and more direct assistance.

Quality of Support: Evaluate the helpfulness and knowledge of the customer support representatives on each platform. Read online reviews or try their support systems directly to assess their responsiveness and ability to resolve your concerns effectively.

Self-Help Resources: Both platforms offer online FAQs and other self-help resources. Compare the comprehensiveness and accessibility of these resources to see if you can find answers to your questions independently before resorting to contacting support.

Budgeting Tools: Kuda’s budgeting tools and spending trackers can be invaluable for users seeking to manage their finances and achieve financial goals. OPay currently lacks dedicated budgeting features.

Bill Reminders: Kuda’s bill reminders help ensure timely payments and avoid late fees. While OPay offers bill payments, built-in reminders might be missing.

Airtime Purchase & Cryptocurrency: OPay caters to users who frequently purchase airtime, pay bills directly through the app, or are interested in exploring cryptocurrency investments. Kuda currently doesn’t offer these specific features.

2. Security

Two-Factor Authentication: Both platforms utilize two-factor authentication for an added layer of security on your account. Compare the specific methods used (SMS, app-based authenticator) and choose the option that best aligns with your security preferences.

Data Encryption: Both Kuda and OPay employ data encryption to safeguard your financial information. However, see their individual security protocols and data privacy policies to gain a deeper understanding of their commitment to protecting your information.

3. Brand Reputation

Transparency & Ethics: Kuda has built a reputation for transparency in its operations and a commitment to ethical business practices. OPay has faced some public criticism regarding data privacy concerns in the past, although they have taken steps to address these issues.

Community Engagement: Consider how each platform interacts with its user base and the overall community perception of its brand values. This can influence your decision if you value transparency, social responsibility, and community engagement from your chosen fintech provider.

Making the Choice

After this thorough exploration of Kuda and OPay, delving into their account features, transaction charges, user experience, and unique value propositions, it’s time to make a confident decision that empowers your financial journey.

For the Savings-Focused User

Prioritizing convenience: Kuda shines with its free transfers, minimalist design, and budgeting tools, making it suitable for managing daily expenses and achieving specific savings goals.

The Feature-Seeking User:

Craving diverse functionalities: OPay’s wider feature set, including airtime purchases, bill payments, and cryptocurrency options, caters to users who value a one-stop shop for various financial needs.

For affordability:

Opay has fewer charges and no card maintenance fees. Unlike Kuda which applies a 50 Naira charge to all deposits of 10,000 Naira or more made into your Kuda account, according to the Federal Government’s Stamp Duty Act.

These are just general recommendations. Your ideal platform hinges on your unique needs and preferences. Consider these additional factors:

Investment goals: Kuda’s fractional stock buying caters to aspiring investors, while OPay focuses on fixed-income securities.

Customer support preferences: Kuda excels with in-app chat and phone support, while OPay relies more on email.

Brand values: Align your choice with the transparency and ethical approach of Kuda, or consider OPay’s efforts to address past data privacy concerns.

FAQs

Is OPay safe to keep money?

OPay implements security measures like data encryption and two-factor authentication. However, like any financial platform, risks are inherent. Conduct your own research and due diligence before making any significant deposits.

Is OPay and Kuda shutting down?

There is no evidence of either platform shutting down or experiencing major operational issues. If you have specific concerns, consult their official websites or contact their customer support for clarification.

Is OPay a Fintech Company?

Yes, OPay is a leading Nigerian fintech company offering mobile payments, digital banking, and other financial services.

Kuda vs. Moniepoint?

Kuda and Moniepoint offer savings accounts, transfers, bill payments, and ATM withdrawals. However, Kuda focuses on individual accounts and investments, while Moniepoint caters to both individuals and businesses with its wider range of services.

Bottom Line

Don’t hesitate to experiment! You can download both Fintech apps, explore their interfaces, and try out their features. This hands-on experience will provide valuable insights into which platform feels most intuitive and aligns seamlessly with your financial habits. Always remember that the “best” platform is one that seamlessly integrates with your lifestyle and financial aspirations.