Physical Address

60 Ekwema Cres, Layout 460281, Imo

Physical Address

60 Ekwema Cres, Layout 460281, Imo

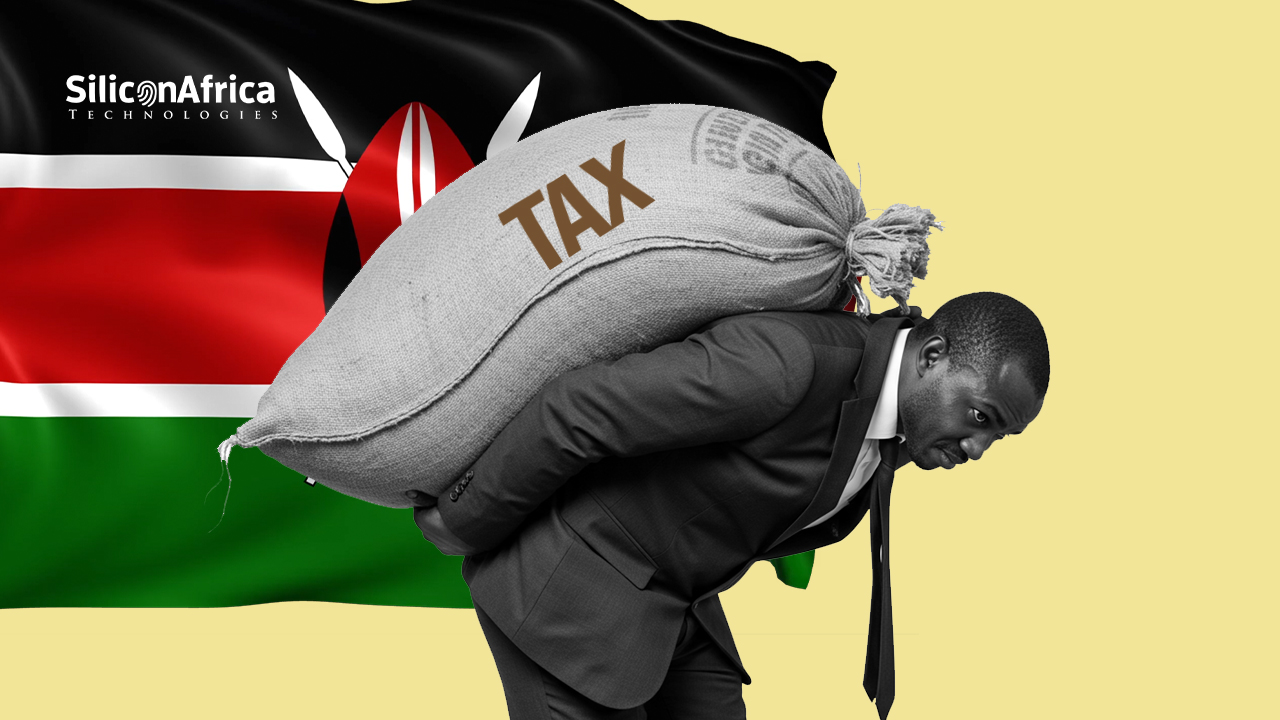

Kenyan CEOs are raising concerns about an economic slowdown in Kenya due to rising costs and tax pressures, which they say are making it harder for businesses to thrive. A recent survey by the Central Bank of Kenya (CBK), which gathered insights from over 1,000 business leaders, revealed that while there is optimism about the country’s economic potential, challenges like high taxes, expensive credit, and unpredictable government policies are creating significant hurdles for companies.

The CEOs highlighted that the cost of doing business in Kenya is climbing at an unsustainable rate. Over the past two years, the government has introduced several tax increases, including higher VAT on essential goods and new levies on mobile money transactions. These measures aim to boost government revenue and reduce public debt but have left businesses struggling to remain competitive. For instance, VAT on fuel was doubled from 8% to 16%, significantly increasing logistics costs for companies.

Peter Mwaura, the CEO of a manufacturing firm in Nairobi, expressed frustration with the lack of tax stability. “There’s no certainty around taxation. The government introduces new levies without consultation, and businesses are forced to react in real time,” he said. Many CEOs echoed this sentiment, calling for more predictable tax policies to enable better long-term planning and investment.

Read Next: Jumia’s Share Price Falls 28% Following Weak 2024 Performance

Another major concern is access to affordable credit. Despite the CBK cutting interest rates three times in the past year to encourage lending, many businesses report that borrowing remains difficult. Banks have been slow to pass on these rate cuts to borrowers, and small and medium-sized enterprises (SMEs) are particularly affected. SMEs form a crucial part of Kenya’s economy, but their growth is being stifled by high interest rates and cautious lending practices by banks.

Susan Wanjiru, an economist at a Nairobi-based investment firm, explained the issue: “The CBK rate cuts haven’t fully trickled down to businesses. Banks are still reluctant to lend to SMEs because of perceived risks.” While some top banks in Kenya have reduced interest rates slightly, many business leaders feel these reductions are not enough to make borrowing affordable.

The survey also revealed that Kenyan CEOs want the government to adopt policies that support business growth. Suggestions include offering tax incentives or holidays for new or innovative businesses, similar to practices in countries like India and Malaysia. Steve Okoth, a tax expert at BDO East Africa, emphasized that such measures could stimulate investment and help businesses reinvest in their operations.

Read Next: Nigerians Consume Over 1 Million Terabytes of Internet Data for the First Time

Despite these challenges, most CEOs remain cautiously optimistic about Kenya’s economic future. Many expect their companies to increase production in the first quarter of 2025 compared to the last quarter of 2024. To sustain growth, businesses are focusing on cost-cutting measures, diversifying their operations, and exploring new markets.

However, business leaders warn that without clear and supportive policies from the government, Kenya’s economic recovery could be slower than expected. Rising costs and tax pressures continue to weigh heavily on companies’ ability to expand and compete effectively.

While Kenyan businesses remain resilient, CEOs stress that long-term growth will require more than just optimism. They urge the government to provide tax certainty and improve access to credit so that businesses can focus on genuine expansion rather than mere survival amidst rising costs and economic pressures.

Was this information useful? Drop a nice comment below. You can also check out other useful contents by following us on X/Twitter @siliconafritech, Instagram @Siliconafricatech, or Facebook @SiliconAfrica.